Over 134 million of American adults gambled in 2025, pushing the national gambling rate past the 50% mark for the first time in history. With recent data revealing that 9 out of 10 Americans find gambling acceptable for themselves and others, that record breaking number is only going to climb.

And since betting has become so mainstream, an important question arises for the majority of the country: does opening a betting account affect your credit rating?

During Problem Gambling Awareness Month, Time2play looked into how placing a wager can hurt or help your score, including the hidden traps you should avoid.

What is a credit score?

A credit score is a financial indicator that reflects a person’s ability to repay debts. Typically ranging from 300 to 850, it is a central concept in the American financial system. The higher the score, the better your chances of obtaining favorable credit terms.

It is most often calculated by FICO (Fair Isaac Corporation) or VantageScore, and influences loan amounts, interest rates, and other financial aspects. For example, a FICO score seen as excellent (760+) can bring your interest rates down to around 6.4% – 6.7% for a mortgage. A fair score between 620 – 639 will likely see that rate rise to 8.2% – 8.8%.

FICO vs VantageScore

While both FICO and VantageScore use a similar scoring system, they weigh different percentages and pull in slightly different data to calculate your credit score.

If you are applying for an education loan, VanguardScore will likely be the one used for measuring your credit history, as it is more fit for younger loaners. For mortgage loans, FICO still remains the staple.

| Feature | FICO score | VantageScore |

|---|---|---|

| Who uses it? | The lender’s standard: Used in over 90% of lending decisions (mortgages, car loans, credit cards). | Consumer and educational: Common on free credit monitoring sites; increasingly used for personal loans and credit cards. |

| History required | 6+ Months: You need a longer track record (and at least one updated account) to generate a score. | 1+ Month: Generates a score quickly; ideal for students or those new to credit. |

| Credit rate shopping window | 45 Days: All inquiries for the same loan type (e.g., mortgage) within 45 days count as one hard pull. | 14 Days: A much tighter window. You must shop for rates quickly to avoid multiple hits to your score. |

| Collections penalties for overdue payments | Stricter: Older versions (often used for mortgages) penalize even paid collections. | Lenient: Generally ignores collection accounts that have been paid in full. |

Sources: Equifax, NerdWallet

It matters how many times a financial institution made inquiries about your credit history (also called hard pull inquiries).

If too many hard pull inquiries are done by lenders throughout a 12 month period, this could cost you around 5 credit points.

The good news is that shopping around for the best credit rate is allowed and expected. This is why multiple hard pulls are grouped together if done in a 45 or 14-day window respectively.

Additionally, collections of overdue payments matter and occur when they have been transferred to a professional debt recovery entity. Even if you do pay, it can take over 7 years to correct your credit score due to collections interference.

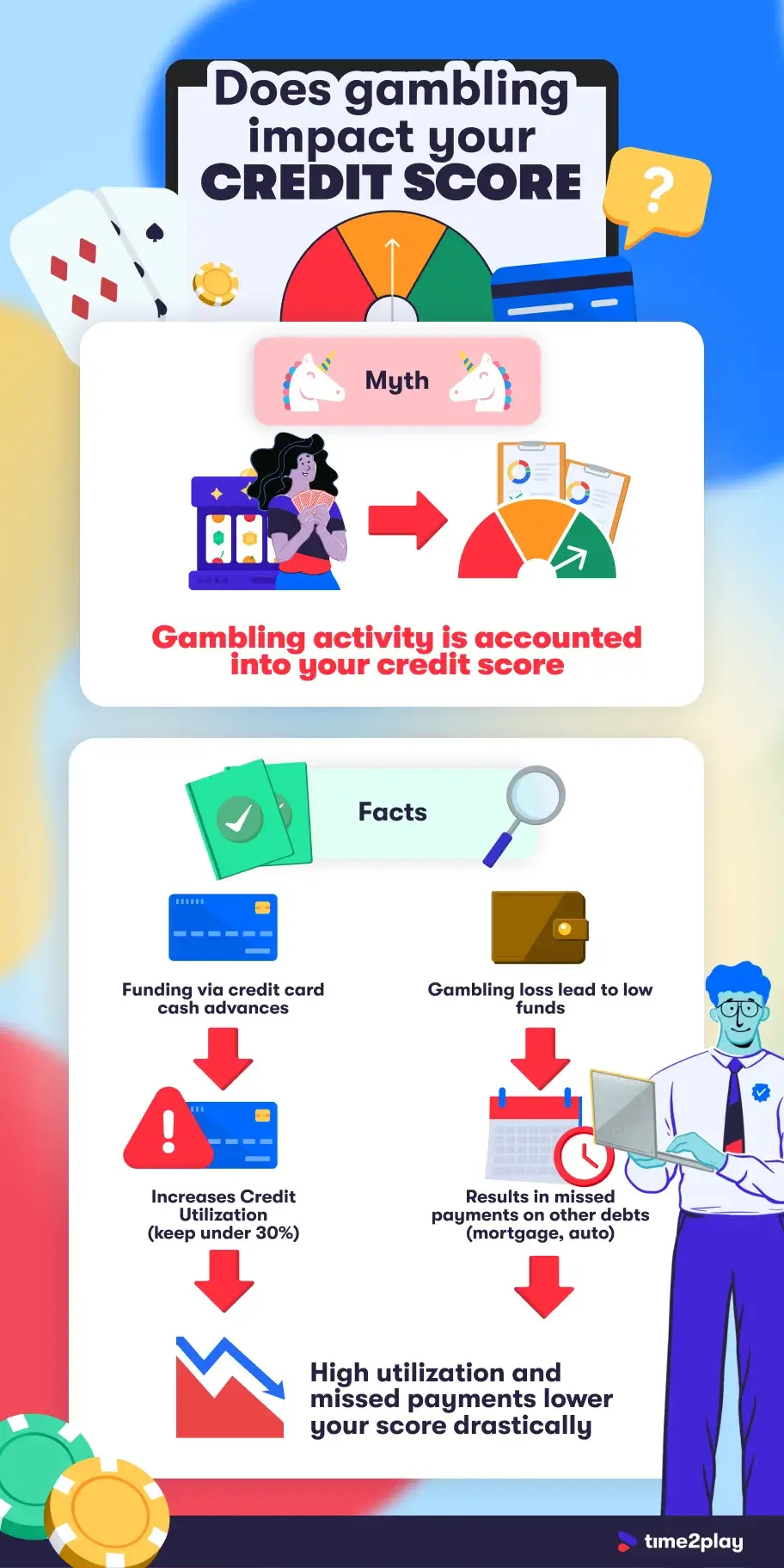

Does gambling affect your credit score?

Gambling does not affect your credit score and it does not show up on your credit report.

Responsible gambling, that is.

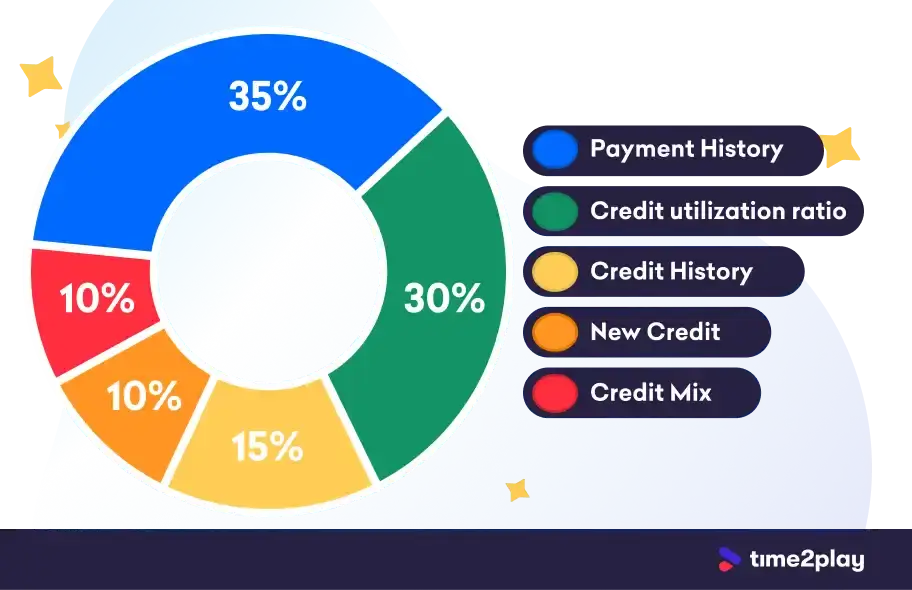

Credit reports monitor factors like credit payment history, credit card utilization, or new credit requests, each weighting in a different proportion:

Gambling can have a derived impact on your credit score in case your wagering activities result in missed loan payments or too large cash advances on your credit cards.

A single missed mortgage, credit card, or car payment can drop your credit score by 50 to 100 points.

In fact, the higher your original credit score, the more points you lose, as credit companies see a high scorer with overdue payments as a sudden increase in risk.

To Credit Bureaus, banks do report credit card activity, but they do not report line-item transaction details. In other words, Credit Bureaus can see you spent $2,000 as cash advance, but they don’t see that you spent it at a casino.

When do cash advances become problematic?

Cash advances become a problem if the borrowed $2,000 represent more than 30% of your available credit card balance. As 30% is the maximum recommended credit card exposure, according to banking institutions, including Capital One.

If you think you can tackle this percentage issue by opening a new one, know that multiple credit card requests can also signal you are credit-hungry, which can lead to denials even if your credit score is high.

But beyond standardized credit score models like FICO or VantageScore, banks use their own internal flagging systems which can evaluate your behavior and analyze the risks of lending money to you.

Even if your bank allows you to gamble online, and as we’ve established, it will not disclose gambling activities to credit bureaus, its computers are programmed to treat gambling transactions carefully.

For banks, gambling activities are seen as a category of payment more likely to lead to defaulted payments.

That is why a long history of responsible gambling will work in your favor, so read on for some easy tips to help you tackle this scenario.

How banks can discover you gamble

When you deposit at an online casino, the transaction is tagged with a Merchant Category Code (usually MCC 7995 for gambling transactions). This code instantly categorizes the spending in the bank’s automated risk calculation algorithms. So, while your bank statement might just say a brand name, the banking system sees a specific risk code.

Thankfully, this data is between you and your bank. This is because banks want to keep their customers to themselves. Disclosing your spending behaviour to other banks or Credit Bureaus, could mean that competition could start targeting you with specific offers to try to get you as a client.

There are two situations where banks may communicate betting transactions to with each other:

- If you use a subsidiary of the same banking corporation.

In this case, make sure you do your background research if you want to keep accounts separate and confidential. - If you need a long term loan, where 2-3 months of bank statements are requested.

In this case, no or low gambling activity plus having a floor account in your balance can demonstrate stability.

What about PayPal?

At PayPal casinos, the way you fund your PayPal account can make a difference. If you deposit using an existing balance in your PayPal wallet, the bank only sees the initial transfer to PayPal (which is neutral). But if you use PayPal as a gateway to top up your casino account, then the bank will be able to record your transaction as a casino deposit.

You may have read about reporting systems like Early Warning Services (EWS) or ChexSystems. These are like credit reports but for deposit and checking accounts.

Banks do share these reports with each other, but they are built exclusively on negative flags like fraud attempts, negative balances or involuntary account closures. They measure your activity up to 5 years back. Here too, if gambling activities did not lead to overdrafts or account abuse, they should not be recorded on your ChexSystems or EWS.

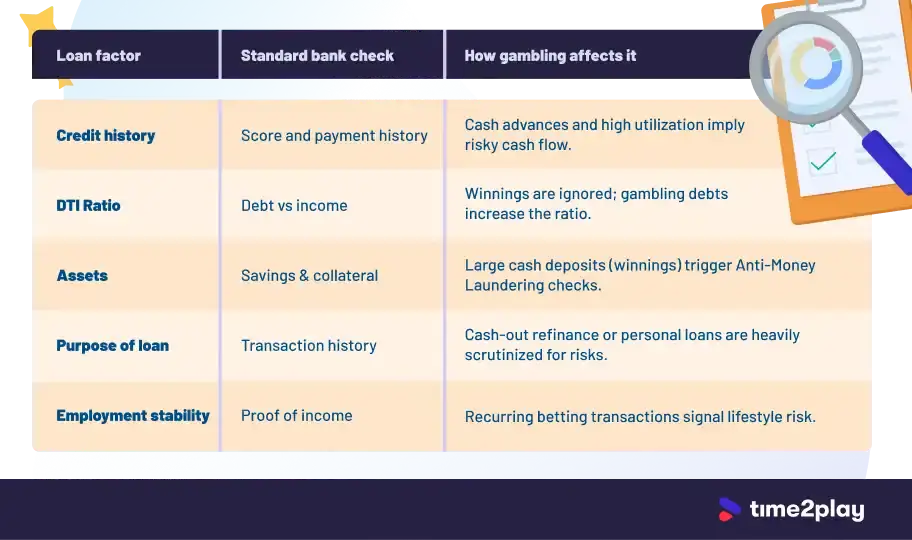

Key factors considered by banks when granting loans and how gambling can affect each

So while gambling is not explicitly listed as a weighting factor when you apply for a bank loan, they can affect their assessment heavily. Here’s how:

- Credit bureau reports: Lenders check your credit score to trace outstanding bad debts, collections, or bankruptcies. Gambling activities such as credit card utilization over 30% or multiple new credit card requests will matter, even if paid to the bank on time.

- Debt-to-Income Ratio (DTI): Banks ensure debt payments will not exceed 36% – 43% of your monthly income. Gambling winnings are not considered an income, and losses are considered debts. If these go beyond the 43% risk score, gambling activities can influence your debit.

- Assets seen as collateral: Banks look for assets you already own (savings, real estate, auto). If your reserves are depleted due to funding gambling activities, or if you suddenly make a deposit from a casino win without being able to prove it was a legitimate casino/source of income, the bank may not see your deposit as a legitimate asset, and can flag it due to money-laundering laws.

- Purpose of loan: Banks assess if the investment is likely to be successful.

If you want to apply for a personal loan or a cash-out refinance, the bank will thoroughly check your activities to assess where that money is going. If they suspect it can go to paying off gambling debts or for more gambling, they will likely deny your loan request and see it as high risk. - Employment stability: You typically need a steady source of income, often verified by up to two years of employment history or tax returns (your W-2s).

This is where gambling can affect you the most, as frequent transactions to crypto exchanges and casino deposits in the last 2-6 months are viewed as financial instability, especially when they lead to insufficient funds or overdrafts. This is seen as unstable behavior.

How to avoid getting a bad credit score when you are gambling

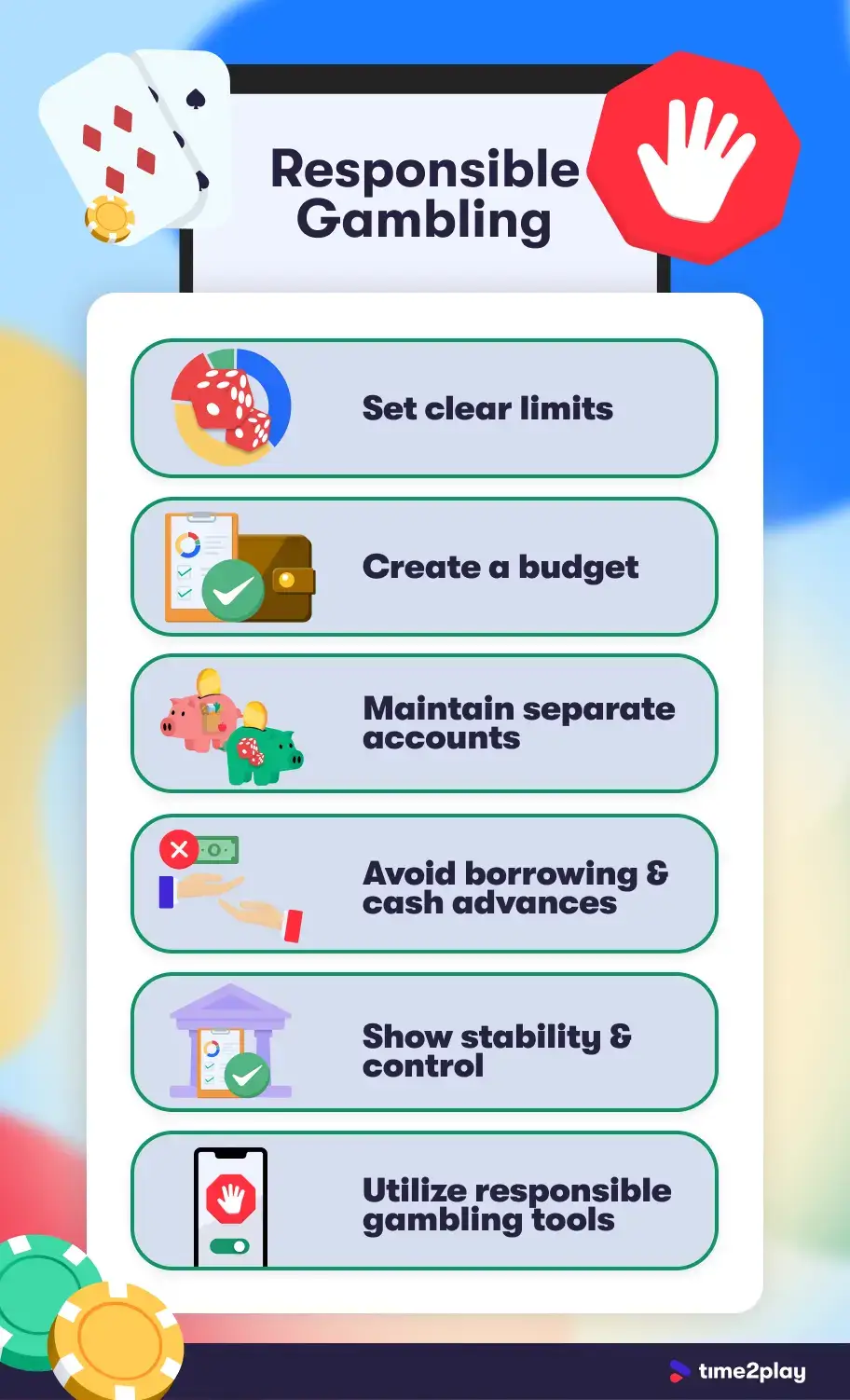

No one likes a bad credit score, especially when trying to get a loan. To avoid damaging your financial health due to gambling, here are some useful tips:

Play responsibly with a limited amount: Gambling should remain a form of entertainment not a form of income. If entertainment activities exceed 5% – 10% of your monthly income, lenders might see it as a lifestyle risk.

- Look at gambling like a utility bill and set aside a monthly unchangeable small amount like $100 – $200 to go to gambling activities.

Use a separate account: It is recommended to keep your savings in a completely separate account from the one used for daily spending or gaming. Ideally, at two different banks.

- Having two accounts gives you privacy, and it also helps maintain a clear separation between funds intended for gambling and those for savings.

Do not borrow to play: This protects your DTI ratio. Never take out a bank loan to chase losses at slots or tables. There is a very high chance you will lose the borrowed money and have no way to pay it back.

- Remember rule #1: look at gambling like a utility bill.

Do not use cash advances: Never use a credit card to gamble. Some banks and now gambling providers will not allow it for gambling anyway, but this activity can be flagged as a cash advance loan which can increase and damage your credit utilization ratio.

- Choose a checking account instead.

Demonstrate stability: While you don’t always need to explain your gambling hobbies to a loan officer, your bank statements must show you are in control. This is more important than a credit score in the final bank decision.

- Overdrafts or non-sufficient funds on your checking account can mean that you have to wait 12 full months before you can make a new loan request.

Do not lend your bank account to others: Do not offer your bank account to family members to play, and do not Venmo or Zelle money to friends to gamble.

- Avoiding these activities will help you prevent triggering money laundering flags or fraud alerts (ChexSystems or EWS checking account checks).

Use gambling blocks: Many banks (like Chase, Bank of America, and Capital One) offer the option to block all transactions to gambling merchants. You can activate this by calling the bank or directly from their mobile apps.

- A gambling block can be perceived positive. It cannot affect your potential loan request and it shows your care to manage risk.

Our take: Gambling goes beyond protecting your credit score

We’ve established that the credit score is not effectively influenced by the pure activity of gambling, however your credit score is not the only one weighting in if your final goal is getting a loan.

Gambling can be seen as a hobby, simple entertainment. But lenders can view it as a risk. Banks see everything, so it is not only your credit score that you need to protect, it’s your overall financial behavior.

You must draw a hard and traceable line between your hobby and your financial persona.

Protect your credit health by playing with small amounts, allocating a separate budget, and try keeping things liquid: no credit cards and no overdrafts.

For further reading, you are invited to our Responsible Gaming section. Here you will find more resources on how to enjoy online gaming safely.

Methodology

To ensure this guide provides accurate financial information to anyone engaged in offline and online betting activities, we reviewed policies and data from recognized financial institutions, credit bureaus, and regulatory bodies.

Our research process focused on separating common financial myths from factual banking mechanics by cross-refferencing information across the following key sources:

- Scoring systems: We analyzed official documentation from Experian, FICO, and VantageScore to understand the exact data points that influence consumer credit scores. This allowed us to verify how credit utilization, hard inquiries, and collections are weighted, and to confirm that gambling activity is not a direct scoring factor.

- Banking and lending risk assessment: We reviewed consumer guidelines and underwriting principles from major lenders and card issuers, including Bank of America, Capital One, and American Express. This helped us map out how banks evaluate Debt-to-Income (DTI) ratios, monitor checking account health via ChexSystems, and assess behavioral risk during the loan approval process.

- Payment processing standards: To explain how financial institutions identify betting transactions behind the scenes, we consulted Visa’s Merchant Data Standards Manual, specifically looking at the application of Merchant Category Codes (MCC 7995) for gambling.

- Regulatory and consumer protection data: We referenced resources from the Consumer Financial Protection Bureau (CFPB) and the Department of Justice (ECOA) to ensure our explanations of credit reporting and fair lending practices align with current federal frameworks.

- Industry statistics: We incorporated recent behavioral data from the American Gaming Association to contextualize the scale of gambling in the US and ground the article in current market realities.

Sources

- American Gambling Association: American Attitudes Towards Gaming https://www.americangaming.org/resources/american-attitudes-towards-gaming/

- myFICO: Credit Education https://www.myfico.com/credit-education

- VantageScore: The Complete Guide to Your VantageScore https://vantagescore.com/consumers/blog/the-complete-guide-to-your-vantagescore

- American Express: Credit Inquiries https://www.americanexpress.com/en-us/credit-cards/credit-intel/credit-inquiries/

- Experian: What Is a Hard Inquiry? https://www.experian.com/blogs/ask-experian/what-is-a-hard-inquiry/

- Consumer Finance.gov Credit Reports and Scores https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/

- VISA: Visa Merchant Data Standards Manual https://usa.visa.com/content/dam/VCOM/download/merchants/visa-merchant-data-standards-manual.pdf

- Capital One: What Is ChexSystems? https://www.capitalone.com/learn-grow/money-management/chexsystems/

- Capital One: What Affects Your Credit Score? https://www.capitalone.com/learn-grow/money-management/what-affects-your-credit-score/

- Bank of America: Factors That Impact Loan Decisions and How to Increase Your Approval Odds https://business.bankofamerica.com/en/resources/factors-that-impact-loan-decisions-and-how-to-increase-your-approval-odds

- Justice.gov: Equal Credit Opportunity Act https://www.justice.gov/crt/equal-credit-opportunity-act-3